General questions about certificates

The underlying is the reference value that determines the performance of the certificate. In principle, all securities traded on a regulated market (= the stock exchange) can also serve as underlyings of certificates - in particular: equities, indices, currencies and futures contracts on commodities.

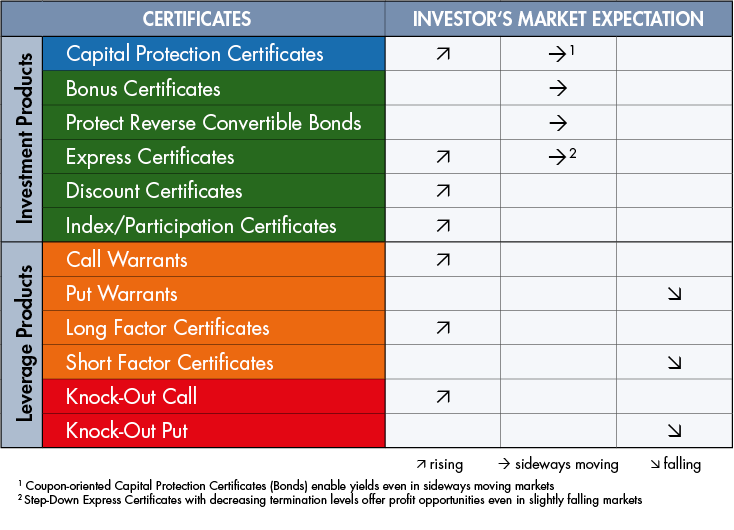

There is the right certificate for every market situation. For a better overview, the following table assigns the appropriate market expectation of the investor to each category of certificates:

No, a significant advantage of certificates is that investments are possible from EUR 1,000 (often even starting from an even smaller amount of money). Thus, even in small securities deposits different kinds of certificates can be kept ("diversification"). The tradability on numerous stock exchanges as well as extensive product documentation ensures maximum transparency.

For investors of any risk appetite - from safety-oriented to speculative - there is a product corresponding to their market expectation. Conservative investors are more likely to prefer investment products with a defensive opportunity / risk ratio (such as Capital Protection Certificates), whereas investors pursuing a very offensive investment strategy often prefer leveraged products to maximally benefit from expected price performance.

To buy certificates you need a securities deposit at your bank. The 12-digit international certificate number, the ISIN, enables you to uniquely identify and trade our products in the securities search of your custodian bank. As an issuer, Raiffeisen Centrobank is the "market maker" in all issued products and, as such, continuously publishes buy and sell prices. As a result, certificates issued by Raiffeisen Centrobank can easily be traded via the stock exchange. Most of the products are listed on the stock exchanges in Vienna, Frankfurt and Stuttgart (US dollar certificates, however, only on the Frankfurt Stock Exchange).

Raiffeisen Centrobank's investment products normally do not incur a management or administration fee. For information about potential charges and fees associated with the trading of certificates, contact your depository bank advisor as they may vary.

No, all expected dividend payments are already taken into account in the product parameters and are therefore paid to the investor indirectly through the yield component of the certificate.

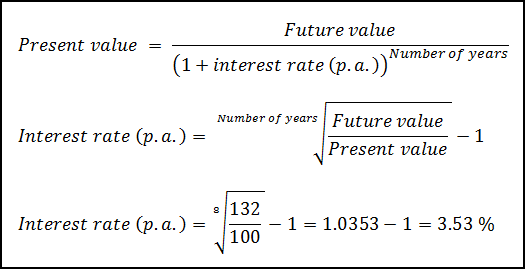

For the annualized interest, the compound interest effect must be taken into account. In order to calculate the annual (= p.a.) interest rate for this example, therefore, the 8th root (corresponding to the term of the certificate - in this case 8 years) must be taken of 132%. This results in a p.a. Interest rate of 3.53%. In the table below, an annual interest rate of 3.53% is compared with a 4% interest rate over a period of 8 years. It can be seen that an interest rate of 4% p.a. after 8 years due to the compounding effect does not equal a total return of 32% but 36.9%.

| Annual interest | Starting value | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | Year 7 | Year 8 |

|---|---|---|---|---|---|---|---|---|---|

| 3.531 % | 100.0 | 103.5 | 107.2 | 111.0 | 114.9 | 118.9 | 123.1 | 127.5 | 132.0 |

| 4.000 % | 100.0 | 104.0 | 108.2 | 112.5 | 117.0 | 121.7 | 126.5 | 131.6 | 136.9 |

(Results in % and rounded to one decimal place.)

The EURO STOXX 50® is a cross-industry equity index that includes the 50 largest companies in the Eurozone by market capitalization and tracks their performance. It is considered one of Europe's leading stock market barometers.

Since an index contains many stocks (the EURO STOXX 50®, for example, contains 50 different stocks), indices have a lower volatility in their price performance compared to single stocks. Major price movements of a single share may be compensated for by other shares included in the index ("diversification") and therefore only change the price of the index to a certain extent (corresponding to the weighting of the share in the index). Equity indices are calculated by an index sponsor - in the case of the EURO STOXX 50® by STOXX Ltd - or in the case of the DAX® by Deutsche Börse. The composition and weighting of the individual shares is rule-based (no active management fees) and is periodically reviewed by the Index Sponsor. Further information can be found on the website of STOXX Ltd.

Certificates make it possible to rule out the market risk associated with a direct investment (capital protection certificates), to reduce them (investment certificates without capital protection) or to leverage on them (leverage certificates).

- Capital Protection Certificates:

In the case of an investment in a Capital Protection Certificate, the investor receives back his invested capital at the end of the term in any case; in addition, there is a potential return if the underlying asset moves in a certain direction (increasing in the end).

- Investment certificates without capital protection:

Bonus Certificates, Protect Reverse Convertibles and Step-Down Express Certificates also provide returns in sideways-moving or slightly decreasing markets. For this, the investor waives price gains above a certain level.

- Leverage certificates:

Turbo or Factor Certificates allow a disproportionate participation in the underlying. Thus losses must be expected in case of sideways moving markets or if the markets move against the market opinion of the investor.

A general advantage of certificates is the tradability, which is guaranteed by the issuer. This ensures that the investor can close his position at any time and sell his certificate at a fair market price.

In addition, some certificates allow easy and efficient investment in otherwise difficult or only with additional effort accessible asset classes. This applies, for example, to raw materials, baskets of shares or exotic individual values.

The disadvantages of certificates include the waiver of dividend payments or any other interest income from the underlyings in return for a specific opportunity to earn. Equally important is the issuer risk as, from a legal perspective, certificates represent bonds issued by banks. This means that in the case of insolvency of the issuer or an official order ("bail-in"), the total loss of the investor's claims may occur.

Details on the opportunities and risks of the different types of certificates can be found in our Certificates Knowledge Compact brochure.

Yes, price gains and all cash flows accruing to investors in Austria (for example, annual fixed interest rates) are subject to the KESt. For investors in other countries, the respective national legal system applies.

Many companies carry out a so-called "cross-listing", i.e. their shares are listed on several stock exchanges. In principle, RCB's certificates are subject to the stock exchange that offers the highest trading volume (= liquidity) in the underlying. In the "Final Terms" of the respective certificate you can find out which stock exchange is specifically used for the observation of the underlying and thus for the price formation / settlement of the certificate.

Bail-in means the participation of creditors of a credit institution (i.e. the investors in their debt securities) in its losses on reorganization or settlement in the event of imminent insolvency. The BRRD was implemented in Austria via the Federal Act on the Recovery and Resolution of Banks (BaSAG) and regulates, among other things, the involvement of creditors of a bank in case of bankruptcy and regulatory action. Holders of Certificates may be affected by such regulatory action in the event of an orderly resolution, i. their claims as holders of certificates vis-à-vis the bank may be written down in whole or in part or certificates may be converted into equity capital of the bank. Further information: www.raiffeisencertificates.at/en/basag

No. Certificates are not deemed to constitute special assets. Certificates issued by RBI (Raiffeisen Bank International) are securities in the form of bearer bond (senior bond) of Raiffeisen Bank International.

Raiffeisen Centrobank continuously issues bid and ask prices for all certificates issued by it (usually on the stock exchanges in Vienna, Frankfurt and Stuttgart). Thus, certificates can be bought on the secondary market at the ask price and sold at the bid price during the trading hours.

Here, a distinction must be made between piece and percentage notes (also called nominal notes). Certificates that are quoted in pieces, such as Bonus Certificates on individual securities, index / participation certificates or discount certificates can often be purchased from just a few euros. For percentage notes, such as Capital Protected Certificates and Reverse Convertibles, the nominal amount is in most cases EUR 1,000, which also represents the minimum investment amount. Information about the tradeable unit for your certificate can be found in the key data on the respective product detail page of the certificate, which can be found at www.raiffeisenzertifikate.at/en. Simply enter the ISIN of your certificate in the search field at the top right of the website.

Capital Protection Certificates

The term Capital Protection Certificate covers all certificates in which the capital employed is protected to a certain percentage (the most common capital protection levels are 90%, 95% and 100%). Guarantee Certificates are only capital protection certificates with at least 100% capital protection. This means that the repayment at maturity is at least 100% of the nominal amount.

Yes, the price of a Guarantee or Capital Protection Certificate may also fall below the level of the capital protection level on the secondary market. The capital protection by Raiffeisen Centrobank is valid only at maturity, i.e. holders of a Guarantee Certificate will receive at least 100% of the nominal amount at the end of the term.

Many investors are generally interested in the stock market, but do not have the appropriate risk tolerance to actually hold shares in their securities deposit. Capital Protection Certificates can be a solution for this situation: they allow participation in rising equity markets while at the same time securing the invested capital. They are therefore particularly suitable for security-oriented investors and represent a possible entry-level product into the world of certificates.

Simply put, a certificate with capital protection in the case of a negative market scenario is to be understood as a fully comprehensive insurance without (100% capital protection) or with a deductible (90% capital protection): If the prices develop contrary to the market opinion of the investor, the repayment takes place at the end of the term, at least to the amount of the capital protection. However, the issuer risk still exists.

For Capital Protection Certificates, Raiffeisen Centrobank differentiates between so-called "Winners" (market expectation: rising) and "Bonds" (market expectation: slightly rising). Winner Certificates allow the investor to participate in the performance of an underlying asset (equity index, commodity, etc.) according to the participation factor up to a maximum amount (the so-called “cap”) at the end of the term, whereas Bond Certificates are particularly strong in sideways or slightly increasing markets. Depending on the structure of the bond certificate, if the underlying at the end of the term quotes at or above the starting value, this is sufficient to achieve a predefined yield.

The willingness of the investor to invest its capital with a medium to long-term investment horizon (for example, 5 to 8 years) makes it possible for certificate issuers to include an attractive performance component in the payout profile in addition to the capital protection.

However, if the investor sells during the term, it is possible that the price of the certificate quotes below 100% and the investor thus realizes losses.

The capital protection is replicated by the issuer with a bond corresponding to the term of the certificate (= debenture bond). Rising interest rates on the bond market lead to corresponding falls in the price of bonds that are already issued, as newly issued bonds offer a higher nominal interest rate and are thus more attractive to the investor.

Since the value of a Capital Protection Certificate is largely determined by the bond component, an increase in interest rates - if all other market parameters remain unchanged - leads to a fall in the price of the certificate. The capital protection at maturity remains intact.

No. The collection of a cap limits the maximum earning potential of a certificate, but in return allows, depending on the type of certificate, higher yields or safety buffers (for Bonus or Express Certificates or Protect Reverse Convertible Bonds) or participation rates (for Capital Protection Certificates).

The withdrawal of a cap thus represents an exchange: The investor waives earnings opportunities above a certain level, but receives an income opportunity.

In addition to the capital protection at the end of the term, “Bonds” or “coupon-oriented” Capital Protection Certificates are equipped with a pre-defined payout level, a fixed interest rate or an annual interest rate opportunity. Either fixed or variable interest payments are made during the term or, at the end of the term, repayment is made in the amount of a defined payout level, provided the underlying has developed accordingly. As a rule, an unchanged / slightly rising price of the underlying is sufficient for the full utilization of the earnings opportunity.

In the case of a “Winner” or “growth-oriented” Capital Protection Certificates, investors participate in the positive performance of the underlying at the end of the term. Thus, these certificates are suitable for investors with a positive market expectation. The participation - the so-called participation - can take different forms:

1. Participation factor: The participation factor indicates the ratio

(e.g., 80%, 120%, etc.) Investors participate in the positive performance of the underlying at maturity. A higher participation factor results in a higher profit potential.

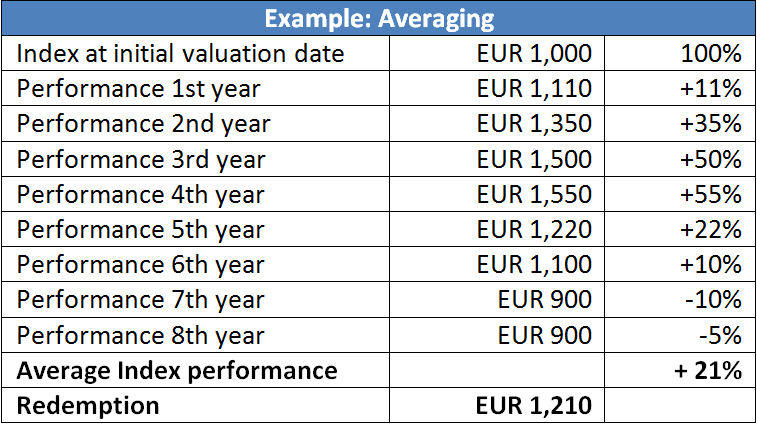

2. Averaging: Investors participate in the average positive performance of the underlying, depending on the level of the participation factor. The price of the underlying is observed at the valuation dates defined at the beginning of the term. The resulting average price is compared with the starting value at the end of the term and - in the case of a positive performance - paid out in accordance with any participation factor.

Bonus Certificates

The payout profile of Bonus Certificates also enables returns in partially declining markets. If, during the observation period, the underlying never touches or falls below the barrier defined at the start of the term, the bonus amount will be paid out at maturity (Bonus Certificates with bonus amount at the end of the term) or the nominal amount (for Bonus Certificates with a fixed interest rate) will be paid out at the end of the term. Whether the underlying quotes below, at or above the starting value at maturity is insignificant.

In return, the investor waives any dividend payments, and the maximum return is limited by the bonus amount or the amount of the interest payments. In the case of a barrier event, the investor is exposed to market risk, as in the case of a direct investment in the underlying without protection.

Even after a barrier event, the maximum redemption amount remains limited to the amount of the bonus amount (cap). Note: "once cap, always cap". In the case of Bonus Certificates with a fixed interest rate, repayment is always effected at a maximum of 100% of the nominal amount.

Reverse Convertible Bonds

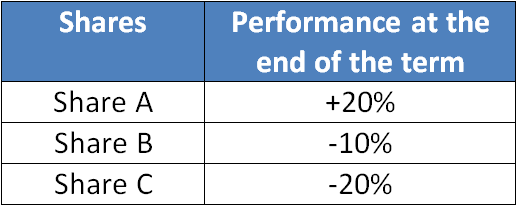

No. In case of a barrier event, the investor will receive only the worst performing share (percentage performance from the starting value (strike) to the closing price of the underlying at the final valuation date) - at the amount defined at the beginning of the term. This means that it does not necessarily have to come to the delivery of the share that caused the barrier event.

Example - physical delivery after barrier violation:

The stock with the worst performance is share C. Therefore, the investor gets only shares of company C in its securities deposit.

No, because the amount of the fixed interest rate, which has accrued since the purchase of the Reverse Convertible Bond, the so-called accrued interest, is already included in the price of the product. This means that the investor buys "too expensive", but receives the entire fixed interest rate on the day of the coupon payment.

In the case of certificates issued by Raiffeisen Centrobank, accrued interest is already included in the price and will therefore be automatically realized when selling at the bid price.

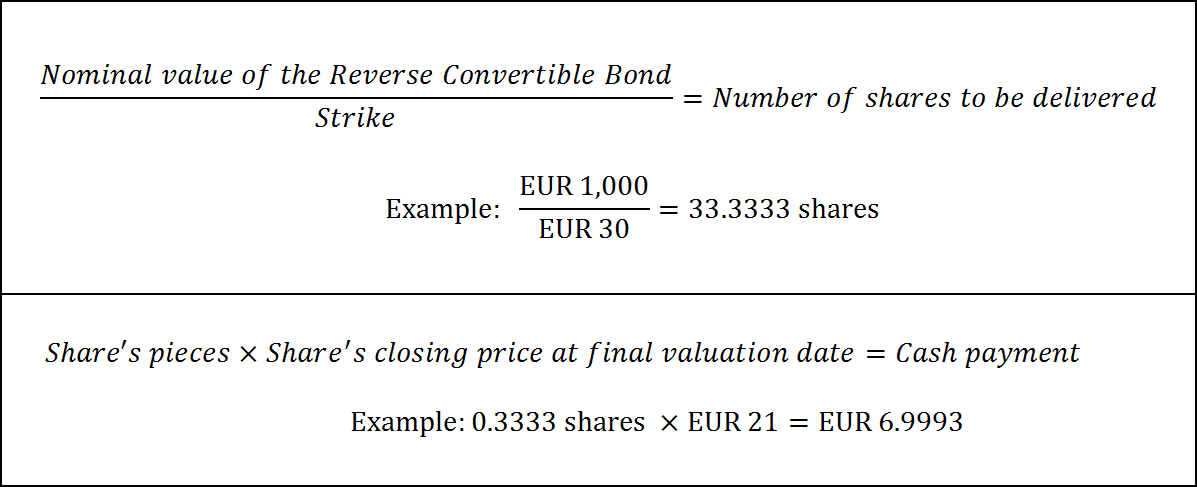

The number of shares defined at the beginning of the term in the case of a physical delivery at the end of the term is calculated as follows:

Basic information:

- Nominal value of the Reverse Convertible Bond: EUR 1,000

- Starting value of the underlying: EUR 30.00

- Closing price of the underlying at the final valuation date: EUR 21.00

At the end of the term, the underlying quotes below its starting value. Therefore, the redemption of the Reverse Convertible Bond is effected by physical delivery at the number defined at the beginning of the term.

In this example, the investor would thus be given the number of 33 shares in his/her securities deposit at a price of EUR 21. The difference to the "whole number" (in this case around EUR 7.00) will be paid out.

No. If an underlying touches/undercuts the barrier during the term, the additional protection mechanism is eliminated and the Barrier Reverse Convertible Bond is analogous to a Traditional Reverse Convertible Bond. In other words, if all underlyings close at or above their respective strike price at the final valuation date, the full nominal amount will be repaid.

This conclusion is not true. To override the protection mechanism of a Barrier Reverse Convertible, it is sufficient if one of the stocks in the equity basket touches or falls below the barrier. An equity basket made up of companies from different sectors increases the industry risk and thus the likelihood that a barrier event will occur. Furthermore, in the case of Reverse Convertible Bonds the "worst-of" principle applies: in the event of a physical delivery, the investor would therefore only receive the share that has the worst performance over the term.

A fundamental principle of the capital market is that the higher the risk, the higher the potential return. Following this principle, Reverse Convertible Bonds allow the product to be designed with more attractive conditions, i.e. with a higher fixed interest rate or a higher safety buffer.

In contrast to a conventional bond, the holder of a Reverse convertible Bond is exposed to the issuer risk as well as to the equity risk. While the fixed interest rate - as the name implies - is always paid out, the amount of the repayment at maturity depends on the performance of the underlying. If applicable, shares in the securities deposit whose market value is less than the originally invested amount will be delivered to the investor, which may result in a loss. To compensate for this additional risk for the investor, the fixed interest rate is significantly above the market interest rate level on the bond market.

The fixed interest payments of a Reverse Convertible Bond represent income from capital assets within the meaning of the capital gains tax (KESt). The KESt is a special collection form of income tax and is deducted directly from the bank or the paying agent and paid to the tax office.

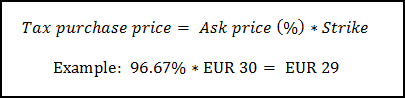

In the case of repayment of the Reverse Convertible Bond in the form of physical delivery, the tax-related purchase price of the shares delivered is significant:

- If the Reverse Convertible Bond was purchased within the subscription period (= primary market), the strike price (closing price of the share to be delivered at the initial valuation date) is used as the purchase price. Thus, the price gains in the share up to the strike price are exempt from the KESt.

- If the purchase of the certificate took place on the secondary market, the ask price at the time of purchase is used to calculate the tax-related purchase price of the share:

The revaluation in the share up to the calculated price (product of ask price and strike price) is tax-free.

Express Certificates

No. If an Express Certificate is prematurely redeemed after the first year of the term, the investor will automatically receive the defined termination price. As a result, no further bid and ask prices will be made for the Express Certificate and a "delisting" of the product from the stock exchanges will take place.

Barrier observation at maturity reduces the risk of a barrier event as it can only occur at the final valuation date. This results in an advantage for the investor.

Other types of certificates

This effect can be explained by the so-called "path dependence". The performance of a Factor Certificate is linked to the performance of the underlying asset, with the daily performance of the certificate being equal to the percentage change in value of the underlying multiplied by the leverage factor set at issuance (excluding interest rate effects). The leverage factor remains constant over the entire term.

The path dependency can be illustrated by the following example with an exemplary Factor Certificate Long with a factor of 3 on oil: For the sake of clarity, it is assumed that both the underlying oil and the certificate are USD 100 on the first day. If, for example, the underlying declines by two percent on one day (from $ 100 to $ 98) and then recovers the equivalent of $ 2 (equal to 2.04%) the next day, the oil price reaches its initial level of $ 100.

The Factor Certificate, however, is losing money: on the first day, the factor 3 paper yields 6% (excluding currency effects) from USD 100 to USD 94. The next day, it wins exactly three times 2.04% (= 6.12%) and thus rises to USD 99.75. Thus, the investor suffers a loss of around 0.25% although the underlying / oil price is unchanged.

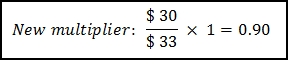

The subscription ratio indicates how many units of the underlying a certificate relates to. A ratio of 0.01 or 1: 100 thus means that you need 100 certificates to represent one unit of the underlying.

All investment options for the commodity oil (e.g. certificates, funds, ETCs) are always based on the oil price traded on the futures market ("futures contract"). The reason for this is obvious: in order to offer products on oil, the issuer must be able to trade the underlying as a hedging transaction. However, as financial institutions do not have appropriate crude oil storage capacity, products cannot be offered on physical oil. The solution is the detour via the futures market, where oil with different delivery dates can be traded as a financial instrument.

RCB's "Open-end" Participation Certificates are based on the underlying futures contract with the shortest remaining term. Before the futures expire, they must always be rolled into the next due date in order to avoid the physical delivery of the underlying. This means that the expiring futures contract will be purchased and the next one due. In order to prevent a price jump in the certificate during the rolling process, the subscription ratio is adjusted. If the next-due futures contract is more expensive than the expiring one, you will receive "less" from this contract - the subscription ratio will be reduced.

Example:

Assuming that the ratio is currently 1: 1, i.e. the certificate corresponds exactly to one unit of the underlying, with the next coming futures contract costing $ 33 and the expiring one costing $ 30:

The subscription ratio would therefore be reduced from 1 to 0.90 in this example.

Investors participate 1: 1 in the future with the shortest remaining maturity between the individual swings. If the future moves between the roles, there will be no change in the price of the certificate, since the change will be neutralized by an adjustment in the ratio. As a result of the rolling process, the investor thus gains neither a profit nor a loss.

Do you have other questions about certificates?

We are happy to take further questions in our FAQ section and answer in detail. Please send your question to

info(at)raiffeisencertificates.com

Your team Raiffeisen Certificates