FAQ - your frequently asked questions

General questions about certificates

Certificates are securities that allow you to invest. They are linked to an underlying asset such as stocks, indices, or commodities. As bearer bonds, they are subject to issuer risk. Raiffeisen Certificates are issued by Raiffeisen Bank International AG (RBI).

Certificates are a special type of bonds where the repayment depends on the value of the underlying. Certificates are transparent, because the payout profile is defined from the beginning. They also offer a balance between opportunity and risk. There are different types of certificates for various market scenarios, such as when the underlying asset rises, remains stable, or falls within a limited range. Our main categories are:

- Investment products: capital protection, bonus, express, discount, and index certificates, as well as reverse convertible bonds

- Leverage products: warrants, factor, and turbo certificates

As with all securities, investing in certificates carries risks, including the potential loss of a significant portion of the invested capital up to a total loss. All certificates are subject to market, issuer, and bail-in risk

Capital protection certificates are suitable for: ⮕ stable or ⬈ rising market development

With the "Bond" payout profile, investors can earn returns when the underlying remains unchanged. "Winner" certificates yield returns when the underlying's price rises.

Bonus certificates are suitable for: ⮕ stable market development

They can also generate returns even if the underlying's price declines slightly. Our "Bonus&Safety" certificates provide a safety buffer of at least 50% at the beginning of the term, offering special partial protection for your capital: even with declines of -50% or more of the underlying, a positive return is possible.

Reverse convertible bonds are suitable for: ⮕ stable market development

Reverse convertible bonds with barrier have a limited protection mechanism down to the barrier.

Express certificates are suitable for: ⮕ stable or ⬈ rising market development

New level express certificates with decreasing termination levels also offer return opportunities in slightly falling markets.

The following applies to other certificate types:

- Discount certificates are suitable for: ⬈ rising market development

- Index/participation certificates are suitable for: ⬈ rising market development

- Long factor certificates, long turbo certificates, call warrants are suitable for: strongly ⮅ rising market development

- Short factor certificates, short turbo certificates, put warrants are suitable for: strongly ⮇ falling market development

All liquid assets traded on an exchange can be used as the underlying for certificates. These include stocks, indices, futures contracts on commodities, or currencies. The underlying significantly determines the performance of the certificate.

A stock index, also known as a share index, reflects the average performance of a defined group of stocks. It represents a "basket" of stocks to illustrate the performance of an industry, market segment, or region. These indices are typically created and calculated by exchanges, independent index providers, or rating agencies.

Well-known stock indices include the S&P 500® (comprising the 500 largest publicly traded companies in the U.S.) and the MSCI® World (tracking the performance of stocks from 23 developed countries, with 1,400 companies included as of February 2025). The EURO STOXX 50®, for example, is a cross-sector stock index that includes the 50 largest companies in the Eurozone by market capitalization and continuously reflects their price performance. In addition to stock indices, there are also investable indices for bonds, commodities, or real estate.

Certificates can largely hedge the market risk associated with a direct investment (capital protection certificates), reduce it (partial protection certificates), or leverage it (leverage products).

- Capital protection certificates: If you invest in a capital protection certificate, you receive your capital back at the end of the term up to the capital protection level, which is usually 100% of the nominal amount or more. The additional opportunity for returns exists, for example, if the underlying asset rises or if an annual interest rate is paid. The capital protection applies exclusively at the end of the term.

- Investment products without capital protection: Bonus certificates, reverse convertible bonds with barrier, and new level express certificates also enable returns when markets remain unchanged or fall to a limited extent. In return, you as an investor forgo price gains above a certain level.

- Leverage certificates: Turbo or factor certificates allow you to benefit more from price movements of the underlying than you could with a direct investment (disproportionate participation). However, if the price moves against your market expectation, you must expect significant capital losses.

A general advantage of certificates is their tradability. You can buy and sell the certificate at the current price during trading hours. Additionally, some certificates provide easy market access and allow investors to invest in asset classes that are otherwise difficult to access or associated with additional effort. This applies, for example, to baskets of selected stocks, emerging market stocks or commodities.

Disadvantages of certificates include the forfeiture of dividend payments or any other interest income from the underlyings in exchange for a specific return opportunity. The issuer risk must also be considered, as certificates are legally bearer bonds issued by banks. This means that in the event of the issuer's insolvency or a regulatory order ("bail-in"), the investor's claims may be completely lost.

You can find more details on the opportunities and risks of different types of certificates in our brochure Certificate Knowledge Compact

No, certificates are suitable for a wide range of people to invest their capital profitably. Capital protection certificates tend to be suitable for security-oriented investors, while more risk-tolerant investors can achieve higher return opportunities with bonus or express certificates. We point out that all certificates carry market, issuer, and bail-in risk. As with all securities, investing in certificates involves risks, including the potential loss of a significant portion of the invested capital up to a total loss.

You need a securities account with your bank to purchase certificates. Using the ISIN (12-digit international identification number), you can identify and trade our investment products or leverage products in the securities search of your custodian bank. As the issuer and market maker, Raiffeisen Bank International AG continuously provides bid and ask prices for all issued products. This allows Raiffeisen certificates to be easily traded on the stock exchange. Most of our certificates are listed on the Vienna and Stuttgart stock exchanges. Raiffeisen Certificates in US dollars are available on the Stuttgart stock exchange.

There is a difference between unit and percentage quotations (also known as nominal quotations):

- Certificates quoted in units include bonus certificates on a single stock, index certificates, or discount certificates. With these, 1 unit can often be purchased for just a few euros.

- In the case of percentage quotations, such as capital protection certificates or reverse convertible bonds, the nominal amount is usually EUR 1,000. This means that investors can invest a minimum amount of 1,000 euros or multiples thereof.

You can find information about the tradable unit for your certificate in the key data on the respective product detail page of the certificate, accessible at raiffeisencertificates.com. To do this, enter the ISIN of your certificate in the search field at the top right of the website.

For Raiffeisen Certificates, there is usually no management or administration fee. Product costs are included in the price of the certificate and can be viewed in the key information document for the respective certificate. Information about possible fees and charges associated with trading certificates can be obtained from your custodian bank, as these may vary.

Under normal market conditions, we continuously provide buy and sell prices for the certificates we issue. This allows certificates to be easily bought at the ask price and sold at the bid price during trading hours. Trading for most of our certificates takes place on the Vienna and Stuttgart stock exchanges.

Therefore, there is no holding period or commitment. However, the respective payout profile of the certificate applies at the end of the certificate's term.

No, with the certificate you will not receive any payouts from the underlying. Dividends and comparable claims from the ownership of the underlying are taken into account in the stucture of the certificate. For example, expected dividends are indirectly passed on through the yield component of the certificate.

To calculate the annual interest rate, the compound interest effect must be considered. For a certificate with a term of 8 years, you take the 8th root of 132%. This results in an annual interest rate of 3.53%.

The following calculation illustrates that an interest rate of 4% per year leads to a total return of 36.9% after 8 years due to the compound interest effect, and not 32% (rounded to one decimal place):

Starting value = 100 %, annual interest rate = 4 %

- 1st year: 100.0 + 4% = 104.0 %

- 2nd year: 104.0 + 4% = 108.2 %

- 3rd year: 108.2 + 4% = 112.5 %

- ... and so on ...

- 8th year: 131.6 + 4 % = 136.9 %

No, certificates are not special assets and are not covered by the Austrian deposit guarantee scheme. Certificates issued by Raiffeisen Bank International (RBI) are securities in the form of bearer bonds (senior bonds) of RBI. Therefore, the buyer of a certificate must also be aware of the issuer risk as well as a possible creditor participation in the event of RBI's insolvency. For more information, please visit raiffeisencertificates.com/bail-in

Bail-in (creditor participation) means that the creditors of a bank, i.e., the investors in its debt securities, are involved in the losses if the bank encounters financial difficulties and becomes insolvent. The Federal Act on the Recovery and Resolution of Banks (Austrian "BASAG" law) specifies how this participation occurs if a bank is in distress and is resolved by the authorities. Holders of certificates may be affected if their claims against the bank are wholly or partially written down or if their certificates are converted into the bank's equity. For more information on bail-in, please visit raiffeisencertificates.com/bail-in

Under Austrian tax law, eligible taxpayers can claim a tax-free investment allowance for profits. Therefore, they must invest in depreciable fixed assets or in securities that are suitable for covering pension provisions (according to § 14 para. 7 no. 4 EStG) and must be dedicated to fixed assets for at least 4 years within the same assessment year.

Criteria for this profit allowance with certificates are:

- Capital protection of 100% or more at the end of the term

- Remaining term of at least 4 years

- Product currency in euros

The bank gains nothing when investors lose. When retail investors purchase a certificate, the bank is never the opponent.

The bank that issues the certificate enables customers to benefit from a certain market development. The bank takes a risk-neutral position itself and hedges its payment obligation through corresponding offsetting transactions in the capital market. The issuer makes money by structuring the certificate and trading it.

Capital Protection Certificates

Capital protection certificates offer investors protection for their invested capital at the maturity date while allowing them to participate in the performance of an underlying asset. The underlying asset can be one or more stocks, indices, or commodities.

Capital protection certificates come with a protection level, such as 90% capital protection, 100% capital protection, or higher. This capital protection applies only at the maturity date and represents the minimum repayment for investors. During the term, prices may fall below the protection level. Selling the capital protection certificate before maturity may result in a loss of part of the invested capital.

The repayment at the maturity date is based on the performance of the underlying asset, such as an index.

- If the underlying asset has performed positively, the repayment for "Winner" certificates aligns with the asset's performance (subject to a potential maximum payout), while for "Bond" certificates, it is made at the predefined payout amount.

- If the underlying asset has performed negatively, the certificate is typically repaid at the level of capital protection.

If a capital protection certificate is sold prior to the maturity date, the price may be below the capital protection level, which can result in a loss of part of the invested capital.

Capital protection certificates of the "Winner" type are particularly suitable for investors who have a positive market outlook for the underlying asset. At the maturity date, investors participate 1:1 in the positive price development of the underlying asset (up to a potential maximum payout).

Capital protection certificates of the "Bond" type are suitable for investors who have a moderate to positive market outlook for the underlying asset. At the maturity date, investors receive a defined amount or the chance for an annual interest rate, depending on the structure, even with sideways or slightly declining prices of the underlying asset.

Für sicherheitsorientierte Anleger:innen, die ihr Kapital schützen und gleichzeitig von Kursanstiegen profitieren wollen, sind Kapitalschutz-Zertifikate interessante Anlageprodukte. Sie bieten eine Möglichkeit, mit geringem Risiko am Kapitalmarkt zu investieren und an der Aktien-Entwicklung teilzuhaben.

- Kurs des Basiswerts: Die Wertentwicklung des zugrunde liegenden Basiswerts (z.B. Aktien, Indizes) beeinflusst den Kurs des Zertifikats während der Laufzeit und vor allem am Laufzeitende.

- Zinsniveau: Wenn die Zinsen steigen oder fallen, beeinflusst das den Wert des Kapitalschutzes im Zertifikat während der Laufzeit.

- Restlaufzeit: Je länger oder kürzer das Zertifikat noch läuft, desto mehr oder weniger kann sich sein Wert ändern.

- Volatilität: Wenn der Kurs des Basiswerts stark schwankt, beeinflusst das den Preis des Zertifikats.

- Bonität des Emittenten: Das Risiko der Zahlungsunfähigkeit des Emittenten kann den Kurs beeinflussen.

- Marktbedingungen: Allgemeine Marktstimmungen und wirtschaftliche Bedingungen spielen ebenfalls eine Rolle.

Ja, der Kurs eines Kapitalschutz-Zertifikats kann während der Laufzeit unter das Kapitalschutz-Level fallen. Der Kapitalschutz greift nur am Ende der Laufzeit, was bedeutet, dass die Anleger:innen am Fälligkeitstag mindestens das Kapitalschutz-Level zurückerhalten, unabhängig von den Kursschwankungen während der Laufzeit. Bitte beachten Sie das Emittenten und Bail-in Risiko. Weitere Informationen finden Sie unter raiffeisenzertifikate.at/basag

Ist beim Kapitalschutz-Zertifikat eine maximale Rückzahlung festgelegt, nehmen Anleger:innen nicht an stärkeren Kursanstiegen des Basiswerts teil. Diese Ertragsobergrenze (auch "Cap") ermöglicht dem Emittenten beispielsweise, ein Zertifikat mit höherem Kapitalschutz oder kürzerer Laufzeit anzubieten.

Somit stellt die Begrenzung einen Tausch dar: Anleger:innen verzichten auf Gewinne oberhalb eines bestimmten Levels, erhalten dafür andere Vorteile.

Als Decrement bezeichnet man den Abzug einer festen, jährlichen Dividende vom Indexwert. Dieser Abzug wird täglich aliquot durchgeführt und kommt bei den MSCI® Decrement-Indizes zur Anwendung. Die tatsächliche Nettodividendenrendite wird 1:1 in die Indexberechnung reinvestiert und im Gegenzug wird eine „feste Dividende“ ( =Decrement) abgezogen, beispielsweise 4,5 % p.a.

Bei Zertifikaten mit einen Decrement-Index als Basiswert ist es uns als Emittent möglich, ein Auszahlungsprofil mit höherer Renditechance zu berechnen.

Bonus Certificates

The payout profile of Bonus Certificates also enables returns in partially declining markets. If, during the observation period, the underlying never touches or falls below the barrier defined at the start of the term, the bonus amount will be paid out at maturity (Bonus Certificates with bonus amount at the end of the term) or the nominal amount (for Bonus Certificates with a fixed interest rate) will be paid out at the end of the term. Whether the underlying quotes below, at or above the starting value at maturity is insignificant.

In return, the investor waives any dividend payments, and the maximum return is limited by the bonus amount or the amount of the interest payments. In the case of a barrier event, the investor is exposed to market risk, as in the case of a direct investment in the underlying without protection.

Even after a barrier event, the maximum redemption amount remains limited to the amount of the bonus amount (cap). Note: "once cap, always cap". In the case of Bonus Certificates with a fixed interest rate, repayment is always effected at a maximum of 100% of the nominal amount.

Express Certificates

No. If an Express Certificate is prematurely redeemed after the first year of the term, the investor will automatically receive the defined termination price. As a result, no further bid and ask prices will be made for the Express Certificate and a "delisting" of the product from the stock exchanges will take place.

Barrier observation at maturity reduces the risk of a barrier event as it can only occur at the final valuation date. This results in an advantage for the investor.

Reverse Convertible Bonds

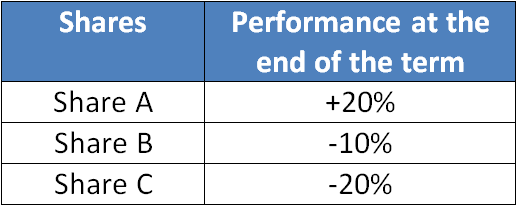

No. In case of a barrier event, the investor will receive only the worst performing share (percentage performance from the starting value (strike) to the closing price of the underlying at the final valuation date) - at the amount defined at the beginning of the term. This means that it does not necessarily have to come to the delivery of the share that caused the barrier event.

Example - physical delivery after barrier violation:

The stock with the worst performance is share C. Therefore, the investor gets only shares of company C in its securities deposit.

No, because the amount of the fixed interest rate, which has accrued since the purchase of the Reverse Convertible Bond, the so-called accrued interest, is already included in the price of the product. This means that the investor buys "too expensive", but receives the entire fixed interest rate on the day of the coupon payment.

In the case of certificates issued by Raiffeisen Certificates, accrued interest is already included in the price and will therefore be automatically realized when selling at the bid price.

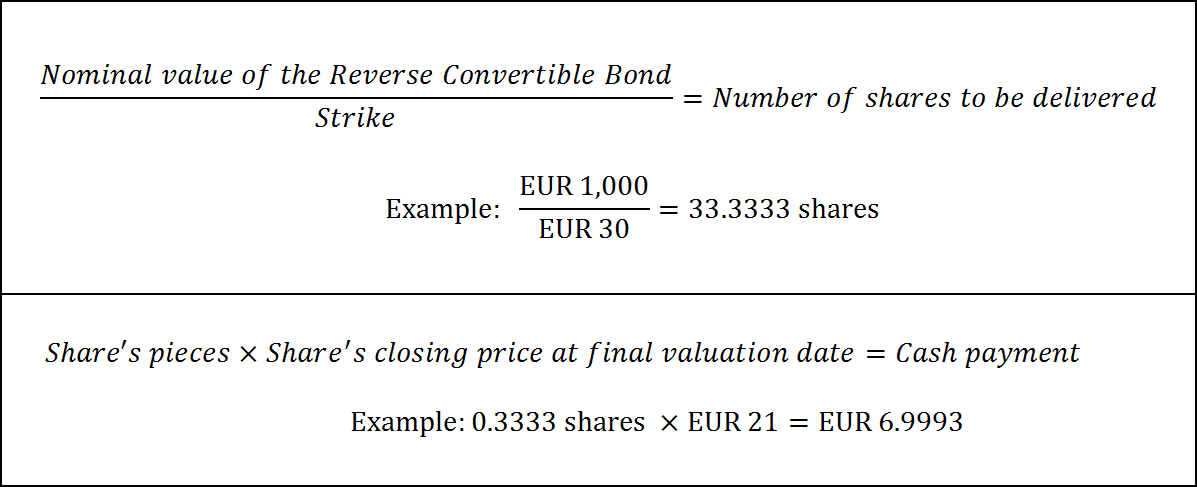

The number of shares defined at the beginning of the term in the case of a physical delivery at the end of the term is calculated as follows:

Basic information:

- Nominal value of the Reverse Convertible Bond: EUR 1,000

- Starting value of the underlying: EUR 30.00

- Closing price of the underlying at the final valuation date: EUR 21.00

At the end of the term, the underlying quotes below its starting value. Therefore, the redemption of the Reverse Convertible Bond is effected by physical delivery at the number defined at the beginning of the term.

In this example, the investor would thus be given the number of 33 shares in his/her securities deposit at a price of EUR 21. The difference to the "whole number" (in this case around EUR 7.00) will be paid out.

No. If an underlying touches/undercuts the barrier during the term, the additional protection mechanism is eliminated and the Barrier Reverse Convertible Bond is analogous to a Traditional Reverse Convertible Bond. In other words, if all underlyings close at or above their respective strike price at the final valuation date, the full nominal amount will be repaid.

This conclusion is not true. To override the protection mechanism of a Barrier Reverse Convertible, it is sufficient if one of the stocks in the equity basket touches or falls below the barrier. An equity basket made up of companies from different sectors increases the industry risk and thus the likelihood that a barrier event will occur. Furthermore, in the case of Reverse Convertible Bonds the "worst-of" principle applies: in the event of a physical delivery, the investor would therefore only receive the share that has the worst performance over the term.

A fundamental principle of the capital market is that the higher the risk, the higher the potential return. Following this principle, Reverse Convertible Bonds allow the product to be designed with more attractive conditions, i.e. with a higher fixed interest rate or a higher safety buffer.

In contrast to a conventional bond, the holder of a Reverse convertible Bond is exposed to the issuer risk as well as to the equity risk. While the fixed interest rate - as the name implies - is always paid out, the amount of the repayment at maturity depends on the performance of the underlying. If applicable, shares in the securities deposit whose market value is less than the originally invested amount will be delivered to the investor, which may result in a loss. To compensate for this additional risk for the investor, the fixed interest rate is significantly above the market interest rate level on the bond market.

The fixed interest payments of a Reverse Convertible Bond represent income from capital assets within the meaning of the capital gains tax (KESt). The KESt is a special collection form of income tax and is deducted directly from the bank or the paying agent and paid to the tax office.

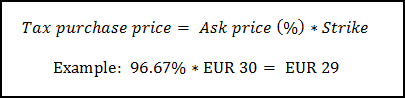

In the case of repayment of the Reverse Convertible Bond in the form of physical delivery, the tax-related purchase price of the shares delivered is significant:

- If the Reverse Convertible Bond was purchased within the subscription period (= primary market), the strike price (closing price of the share to be delivered at the initial valuation date) is used as the purchase price. Thus, the price gains in the share up to the strike price are exempt from the KESt.

- If the purchase of the certificate took place on the secondary market, the ask price at the time of purchase is used to calculate the tax-related purchase price of the share:

The revaluation in the share up to the calculated price (product of ask price and strike price) is tax-free.

Other types of certificates

This effect can be explained by the so-called "path dependence". The performance of a Factor Certificate is linked to the performance of the underlying asset, with the daily performance of the certificate being equal to the percentage change in value of the underlying multiplied by the leverage factor set at issuance (excluding interest rate effects). The leverage factor remains constant over the entire term.

The path dependency can be illustrated by the following example with an exemplary Factor Certificate Long with a factor of 3 on oil: For the sake of clarity, it is assumed that both the underlying oil and the certificate are USD 100 on the first day. If, for example, the underlying declines by two percent on one day (from $ 100 to $ 98) and then recovers the equivalent of $ 2 (equal to 2.04%) the next day, the oil price reaches its initial level of $ 100.

The Factor Certificate, however, is losing money: on the first day, the factor 3 paper yields 6% (excluding currency effects) from USD 100 to USD 94. The next day, it wins exactly three times 2.04% (= 6.12%) and thus rises to USD 99.75. Thus, the investor suffers a loss of around 0.25% although the underlying / oil price is unchanged.

The subscription ratio indicates how many units of the underlying a certificate relates to. A ratio of 0.01 or 1: 100 thus means that you need 100 certificates to represent one unit of the underlying.

All investment options for the commodity oil (e.g. certificates, funds, ETCs) are always based on the oil price traded on the futures market ("futures contract"). The reason for this is obvious: in order to offer products on oil, the issuer must be able to trade the underlying as a hedging transaction. However, as financial institutions do not have appropriate crude oil storage capacity, products cannot be offered on physical oil. The solution is the detour via the futures market, where oil with different delivery dates can be traded as a financial instrument.

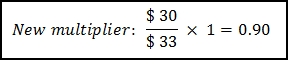

Our "Open-end" Participation Certificates are based on the underlying futures contract with the shortest remaining term. Before the futures expire, they must always be rolled into the next due date in order to avoid the physical delivery of the underlying. This means that the expiring futures contract will be purchased and the next one due. In order to prevent a price jump in the certificate during the rolling process, the subscription ratio is adjusted. If the next-due futures contract is more expensive than the expiring one, you will receive "less" from this contract - the subscription ratio will be reduced.

Example:

Assuming that the ratio is currently 1: 1, i.e. the certificate corresponds exactly to one unit of the underlying, with the next coming futures contract costing $ 33 and the expiring one costing $ 30:

The subscription ratio would therefore be reduced from 1 to 0.90 in this example.

Investors participate 1: 1 in the future with the shortest remaining maturity between the individual swings. If the future moves between the roles, there will be no change in the price of the certificate, since the change will be neutralized by an adjustment in the ratio. As a result of the rolling process, the investor thus gains neither a profit nor a loss.

Do you have other questions about certificates?

We are happy to take further questions in our FAQ section and answer in detail. Please send your question to

info(at)raiffeisencertificates.com

Your Raiffeisen Certificates team