FAQ - vaše často kladené otázky

Všeobecné otázky o certifikátoch

Certificates are securities that allow you to invest. They are linked to an underlying asset such as stocks, indices, or commodities. As bearer bonds, they are subject to issuer risk. Raiffeisen Certificates are issued by Raiffeisen Bank International AG (RBI).

Certificates are a special type of bonds where the repayment depends on the value of the underlying. Certificates are transparent, because the payout profile is defined from the beginning. They also offer a balance between opportunity and risk. There are different types of certificates for various market scenarios, such as when the underlying asset rises, remains stable, or falls within a limited range. Our main categories are:

- Investment products: capital protection, bonus, express, discount, and index certificates, as well as reverse convertible bonds

- Leverage products: warrants, factor, and turbo certificates

As with all securities, investing in certificates carries risks, including the potential loss of a significant portion of the invested capital up to a total loss. All certificates are subject to market, issuer, and bail-in risk

Capital protection certificates are suitable for: ⮕ stable or ⬈ rising market development

With the "Bond" payout profile, investors can earn returns when the underlying remains unchanged. "Winner" certificates yield returns when the underlying's price rises.

Bonus certificates are suitable for: ⮕ stable market development

They can also generate returns even if the underlying's price declines slightly. Our "Bonus&Safety" certificates provide a safety buffer of at least 50% at the beginning of the term, offering special partial protection for your capital: even with declines of -50% or more of the underlying, a positive return is possible.

Reverse convertible bonds are suitable for: ⮕ stable market development

Reverse convertible bonds with barrier have a limited protection mechanism down to the barrier.

Express certificates are suitable for: ⮕ stable or ⬈ rising market development

New level express certificates with decreasing termination levels also offer return opportunities in slightly falling markets.

The following applies to other certificate types:

- Discount certificates are suitable for: ⬈ rising market development

- Index/participation certificates are suitable for: ⬈ rising market development

- Long factor certificates, long turbo certificates, call warrants are suitable for: strongly ⮅ rising market development

- Short factor certificates, short turbo certificates, put warrants are suitable for: strongly ⮇ falling market development

All liquid assets traded on an exchange can be used as the underlying for certificates. These include stocks, indices, futures contracts on commodities, or currencies. The underlying significantly determines the performance of the certificate.

A stock index, also known as a share index, reflects the average performance of a defined group of stocks. It represents a "basket" of stocks to illustrate the performance of an industry, market segment, or region. These indices are typically created and calculated by exchanges, independent index providers, or rating agencies.

Well-known stock indices include the S&P 500® (comprising the 500 largest publicly traded companies in the U.S.) and the MSCI® World (tracking the performance of stocks from 23 developed countries, with 1,400 companies included as of February 2025). The EURO STOXX 50®, for example, is a cross-sector stock index that includes the 50 largest companies in the Eurozone by market capitalization and continuously reflects their price performance. In addition to stock indices, there are also investable indices for bonds, commodities, or real estate.

Certificates can largely hedge the market risk associated with a direct investment (capital protection certificates), reduce it (partial protection certificates), or leverage it (leverage products).

- Capital protection certificates: If you invest in a capital protection certificate, you receive your capital back at the end of the term up to the capital protection level, which is usually 100% of the nominal amount or more. The additional opportunity for returns exists, for example, if the underlying asset rises or if an annual interest rate is paid. The capital protection applies exclusively at the end of the term.

- Investment products without capital protection: Bonus certificates, reverse convertible bonds with barrier, and new level express certificates also enable returns when markets remain unchanged or fall to a limited extent. In return, you as an investor forgo price gains above a certain level.

- Leverage certificates: Turbo or factor certificates allow you to benefit more from price movements of the underlying than you could with a direct investment (disproportionate participation). However, if the price moves against your market expectation, you must expect significant capital losses.

A general advantage of certificates is their tradability. You can buy and sell the certificate at the current price during trading hours. Additionally, some certificates provide easy market access and allow investors to invest in asset classes that are otherwise difficult to access or associated with additional effort. This applies, for example, to baskets of selected stocks, emerging market stocks or commodities.

Disadvantages of certificates include the forfeiture of dividend payments or any other interest income from the underlyings in exchange for a specific return opportunity. The issuer risk must also be considered, as certificates are legally bearer bonds issued by banks. This means that in the event of the issuer's insolvency or a regulatory order ("bail-in"), the investor's claims may be completely lost.

You can find more details on the opportunities and risks of different types of certificates in our brochure Certificate Knowledge Compact

No, certificates are suitable for a wide range of people to invest their capital profitably. Capital protection certificates tend to be suitable for security-oriented investors, while more risk-tolerant investors can achieve higher return opportunities with bonus or express certificates. We point out that all certificates carry market, issuer, and bail-in risk. As with all securities, investing in certificates involves risks, including the potential loss of a significant portion of the invested capital up to a total loss.

You need a securities account with your bank to purchase certificates. Using the ISIN (12-digit international identification number), you can identify and trade our investment products or leverage products in the securities search of your custodian bank. As the issuer and market maker, Raiffeisen Bank International AG continuously provides bid and ask prices for all issued products. This allows Raiffeisen certificates to be easily traded on the stock exchange. Most of our certificates are listed on the Vienna and Stuttgart stock exchanges. Raiffeisen Certificates in US dollars are available on the Stuttgart stock exchange.

There is a difference between unit and percentage quotations (also known as nominal quotations):

- Certificates quoted in units include bonus certificates on a single stock, index certificates, or discount certificates. With these, 1 unit can often be purchased for just a few euros.

- In the case of percentage quotations, such as capital protection certificates or reverse convertible bonds, the nominal amount is usually EUR 1,000. This means that investors can invest a minimum amount of 1,000 euros or multiples thereof.

You can find information about the tradable unit for your certificate in the key data on the respective product detail page of the certificate, accessible at raiffeisencertificates.com. To do this, enter the ISIN of your certificate in the search field at the top right of the website.

For Raiffeisen Certificates, there is usually no management or administration fee. Product costs are included in the price of the certificate and can be viewed in the key information document for the respective certificate. Information about possible fees and charges associated with trading certificates can be obtained from your custodian bank, as these may vary.

Under normal market conditions, we continuously provide buy and sell prices for the certificates we issue. This allows certificates to be easily bought at the ask price and sold at the bid price during trading hours. Trading for most of our certificates takes place on the Vienna and Stuttgart stock exchanges.

Therefore, there is no holding period or commitment. However, the respective payout profile of the certificate applies at the end of the certificate's term.

No, with the certificate you will not receive any payouts from the underlying. Dividends and comparable claims from the ownership of the underlying are taken into account in the stucture of the certificate. For example, expected dividends are indirectly passed on through the yield component of the certificate.

To calculate the annual interest rate, the compound interest effect must be considered. For a certificate with a term of 8 years, you take the 8th root of 132%. This results in an annual interest rate of 3.53%.

The following calculation illustrates that an interest rate of 4% per year leads to a total return of 36.9% after 8 years due to the compound interest effect, and not 32% (rounded to one decimal place):

Starting value = 100 %, annual interest rate = 4 %

- 1st year: 100.0 + 4% = 104.0 %

- 2nd year: 104.0 + 4% = 108.2 %

- 3rd year: 108.2 + 4% = 112.5 %

- ... and so on ...

- 8th year: 131.6 + 4 % = 136.9 %

No, certificates are not special assets and are not covered by the Austrian deposit guarantee scheme. Certificates issued by Raiffeisen Bank International (RBI) are securities in the form of bearer bonds (senior bonds) of RBI. Therefore, the buyer of a certificate must also be aware of the issuer risk as well as a possible creditor participation in the event of RBI's insolvency. For more information, please visit raiffeisencertificates.com/bail-in

Bail-in (creditor participation) means that the creditors of a bank, i.e., the investors in its debt securities, are involved in the losses if the bank encounters financial difficulties and becomes insolvent. The Federal Act on the Recovery and Resolution of Banks (Austrian "BASAG" law) specifies how this participation occurs if a bank is in distress and is resolved by the authorities. Holders of certificates may be affected if their claims against the bank are wholly or partially written down or if their certificates are converted into the bank's equity. For more information on bail-in, please visit raiffeisencertificates.com/bail-in

Under Austrian tax law, eligible taxpayers can claim a tax-free investment allowance for profits. Therefore, they must invest in depreciable fixed assets or in securities that are suitable for covering pension provisions (according to § 14 para. 7 no. 4 EStG) and must be dedicated to fixed assets for at least 4 years within the same assessment year.

Criteria for this profit allowance with certificates are:

- Capital protection of 100% or more at the end of the term

- Remaining term of at least 4 years

- Product currency in euros

The bank gains nothing when investors lose. When retail investors purchase a certificate, the bank is never the opponent.

The bank that issues the certificate enables customers to benefit from a certain market development. The bank takes a risk-neutral position itself and hedges its payment obligation through corresponding offsetting transactions in the capital market. The issuer makes money by structuring the certificate and trading it.

Zaistené certifikáty

Capital protection certificates offer investors protection for their invested capital at the maturity date while allowing them to participate in the performance of an underlying asset. The underlying asset can be one or more stocks, indices, or commodities.

Capital protection certificates come with a protection level, such as 90% capital protection, 100% capital protection, or higher. This capital protection applies only at the maturity date and represents the minimum repayment for investors. During the term, prices may fall below the protection level. Selling the capital protection certificate before maturity may result in a loss of part of the invested capital.

The repayment at the maturity date is based on the performance of the underlying asset, such as an index.

- If the underlying asset has performed positively, the repayment for "Winner" certificates aligns with the asset's performance (subject to a potential maximum payout), while for "Bond" certificates, it is made at the predefined payout amount.

- If the underlying asset has performed negatively, the certificate is typically repaid at the level of capital protection.

If a capital protection certificate is sold prior to the maturity date, the price may be below the capital protection level, which can result in a loss of part of the invested capital.

Capital protection certificates of the "Winner" type are particularly suitable for investors who have a positive market outlook for the underlying asset. At the maturity date, investors participate 1:1 in the positive price development of the underlying asset (up to a potential maximum payout).

Capital protection certificates of the "Bond" type are suitable for investors who have a moderate to positive market outlook for the underlying asset. At the maturity date, investors receive a defined amount or the chance for an annual interest rate, depending on the structure, even with sideways or slightly declining prices of the underlying asset.

Für sicherheitsorientierte Anleger:innen, die ihr Kapital schützen und gleichzeitig von Kursanstiegen profitieren wollen, sind Kapitalschutz-Zertifikate interessante Anlageprodukte. Sie bieten eine Möglichkeit, mit geringem Risiko am Kapitalmarkt zu investieren und an der Aktien-Entwicklung teilzuhaben.

- Kurs des Basiswerts: Die Wertentwicklung des zugrunde liegenden Basiswerts (z.B. Aktien, Indizes) beeinflusst den Kurs des Zertifikats während der Laufzeit und vor allem am Laufzeitende.

- Zinsniveau: Wenn die Zinsen steigen oder fallen, beeinflusst das den Wert des Kapitalschutzes im Zertifikat während der Laufzeit.

- Restlaufzeit: Je länger oder kürzer das Zertifikat noch läuft, desto mehr oder weniger kann sich sein Wert ändern.

- Volatilität: Wenn der Kurs des Basiswerts stark schwankt, beeinflusst das den Preis des Zertifikats.

- Bonität des Emittenten: Das Risiko der Zahlungsunfähigkeit des Emittenten kann den Kurs beeinflussen.

- Marktbedingungen: Allgemeine Marktstimmungen und wirtschaftliche Bedingungen spielen ebenfalls eine Rolle.

Ja, der Kurs eines Kapitalschutz-Zertifikats kann während der Laufzeit unter das Kapitalschutz-Level fallen. Der Kapitalschutz greift nur am Ende der Laufzeit, was bedeutet, dass die Anleger:innen am Fälligkeitstag mindestens das Kapitalschutz-Level zurückerhalten, unabhängig von den Kursschwankungen während der Laufzeit. Bitte beachten Sie das Emittenten und Bail-in Risiko. Weitere Informationen finden Sie unter raiffeisenzertifikate.at/basag

Ist beim Kapitalschutz-Zertifikat eine maximale Rückzahlung festgelegt, nehmen Anleger:innen nicht an stärkeren Kursanstiegen des Basiswerts teil. Diese Ertragsobergrenze (auch "Cap") ermöglicht dem Emittenten beispielsweise, ein Zertifikat mit höherem Kapitalschutz oder kürzerer Laufzeit anzubieten.

Somit stellt die Begrenzung einen Tausch dar: Anleger:innen verzichten auf Gewinne oberhalb eines bestimmten Levels, erhalten dafür andere Vorteile.

Als Decrement bezeichnet man den Abzug einer festen, jährlichen Dividende vom Indexwert. Dieser Abzug wird täglich aliquot durchgeführt und kommt bei den MSCI® Decrement-Indizes zur Anwendung. Die tatsächliche Nettodividendenrendite wird 1:1 in die Indexberechnung reinvestiert und im Gegenzug wird eine „feste Dividende“ ( =Decrement) abgezogen, beispielsweise 4,5 % p.a.

Bei Zertifikaten mit einen Decrement-Index als Basiswert ist es uns als Emittent möglich, ein Auszahlungsprofil mit höherer Renditechance zu berechnen.

Bonusové certifikáty

Výplatný profil bonusových certifikátov umožňuje výnosy aj na čiastočne klesajúcich trhoch. Ak sa počas sledovaného obdobia podkladové aktívum nikdy nedotkne bariéry definovanej na začiatku trvania alebo klesne pod ňu, bonusová suma bude vyplatená pri splatnosti (bonusové certifikáty s bonusovou sumou na konci trvania) alebo nominálna suma (v prípade bonusových certifikátov s pevnou úrokovou sadzbou) bude vyplatená na konci trvania. Nie je dôležité, či sa podkladové aktívum v čase splatnosti bude nechádzať pod, na alebo nad úvodnou hodnotou.

Avšak, investor sa vzdáva akýchkoľvek dividendových platieb a maximálny výnos je limitovaný výškou bonusu alebo úrokov. V prípade bariérovej udalosti je investor vystavený trhovému riziku ako v prípade priamej investície do podkladového aktíva bez akejkoľvek ochrany.

Aj po bariérovej udalosti zostáva maximálna suma vyplatenia obmedzená výškou bonusu (cap). Poznámka: „raz cap, vždy cap“. V prípade bonusových certifikátov s pevnou úrokovou sadzbou sa splatenie uskutočňuje vždy maximálne vo výške 100 % nominálnej hodnoty.

Expresné certifikáty

Nie. Ak je expresný certifikát predčasne splatený po prvom roku platnosti, investor automaticky dostane stanovenú sumu za ukončenie splatnosti. V dôsledku toho sa pre expresný certifikát nebudú vytvárať žiadne ďalšie nákupné a predajné ceny a dôjde k „vyradeniu“ produktu z burzy cenných papierov.

Pozorovanie bariéry pri splatnosti znižuje riziko bariérovej udalosti, keďže môže nastať len v deň finálneho ocenenia. Z toho vyplýva výhoda pre investora.

Reverzne konvertibilné dlhopisy

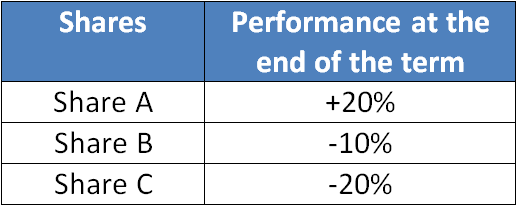

Nie. V prípade bariérovej udalosti investor obdrží iba akciu s najhoršou výkonnosťou (percentuálny výkon od úvodnej hodnoty (strike) po uzatváraciu cenu podkladového aktíva k dňu finálneho ocenenia) – v hodnote určenej na začiatku doby trvania. To znamená, že nemusí nevyhnutne dôjsť k dodaniu akcie, ktorá spôsobila bariérovú udalosť.

Príklad - doručenie po porušení bariéry:

Akcia s najhoršou výkonnosťou je akcia C. Investor preto vo svojom depozite cenných papierov získa len akcie spoločnosti C.

Nie, pretože hodnota pevnej úrokovej sadzby, ktorá vznikla od kúpy reverzného konvertibilného dlhopisu, tzv. naakumulovaný úrok, je už zahrnutá v cene produktu. To znamená, že investor kupuje „draho“, ale v deň výplaty kupónu dostane celú pevnú úrokovú sadzbu.

V prípade certifikátov vydaných spoločnosťou Raiffeisen Certificates sú naakumulované úroky už zahrnuté v cene, a preto sa automaticky realizujú pri predaji za nákupnú cenu.

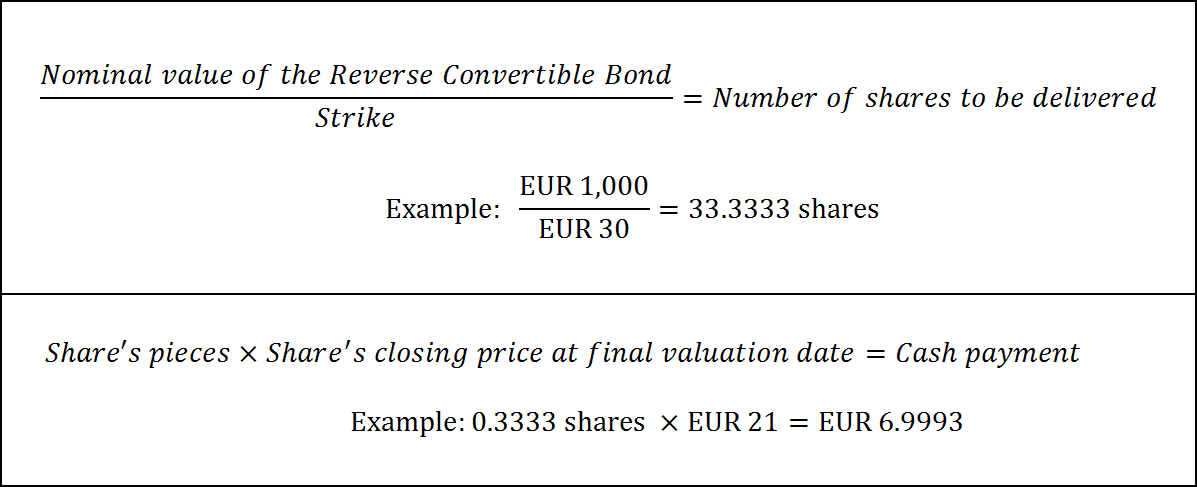

Počet akcií definovaný na začiatku trvania v prípade dodávky na konci trvania sa vypočíta takto:

Základné informácie:

- Nominálna hodnota reverzne konvertibilného dlhopisu: 1.000 EUR

- Počiatočná hodnota podkladového aktíva: 30,00 EUR

- Uzatváracia cena podkladového aktíva v deň finálneho ocenenia: 21,00 EUR

Na konci trvania sa podkladové aktívum nachádza pod jeho úvodnou hodnotu. Splatenie reverzne konvertibilného dlhopisu sa preto uskutoční dodaním v počte stanovenom na začiatku trvania.

V tomto príklade by teda investor dostal 33 akcií zo svojho vkladu cenných papierov za cenu 21 EUR. Rozdiel do „celého čísla“ (v tomto prípade približne 7,00 EUR) bude vyplatený.

Nie. Ak sa podkladové aktívum dosiahne/naruší bariéru počas doby splatnosti, dodatočný ochranný mechanizmus sa zruší a bariérový reverzne konvertibilný dlhopis je prakticky rovnaký ako tradičný reverzne konvertibilný dlhopis. Inými slovami, ak sa všetky podkladové aktíva v deň finálneho ocenenia nachádzajú na alebo nad úrovňou svojej príslušnej ceny, splatí sa celá nominálna hodnota.

Tento záver nie je pravdivý. Na zrušenie ochranného mechanizmu bariérového reverzne konvertibilného dlhopisu stačí, ak sa jedna z akcií v koši akcií dotkne bariéry alebo klesne pod ňu. Akciový kôš zložený zo spoločností z rôznych sektorov zvyšuje odvetvové riziko, a tým aj pravdepodobnosť, že nastane bariérová udalosť. Okrem toho sa v prípade reverzne konvertibilných dlhopisov uplatňuje princíp „worst of“: v prípade fyzického dodania by teda investor dostal iba akciu, ktorá má počas doby splatnosti najhoršiu výkonnosť.

Základným princípom kapitálového trhu je, že čím vyššie je riziko, tým vyšší je potenciálny výnos. V súlade s touto zásadou umožňujú reverzne konvertibilné dlhopisy navrhnúť produkt s atraktívnejšími podmienkami, t. j. s vyššou pevnou úrokovou sadzbou alebo vyššou bezpečnostnou rezervou.

Na rozdiel od bežného dlhopisu je držiteľ reverzne konvertibilného dlhopisu vystavený riziku emitenta, ako aj akciovému riziku. Zatiaľ čo pevná úroková sadzba - ako naznačuje názov - sa vypláca vždy, výška splátky pri splatnosti závisí od výkonnosti podkladového aktíva. Prípadne sa investorovi dodajú akcie z depozitu cenných papierov, ktorých trhová hodnota je nižšia ako pôvodne investovaná suma, čo môže viesť k strate. Na kompenzáciu tohto dodatočného rizika pre investora je pevná úroková sadzba výrazne vyššia ako úroveň trhovej úrokovej sadzby na trhu s dlhopismi.

Pevné úrokové platby reverzne konvertibilného dlhopisu predstavujú príjem z kapitálových aktív v zmysle dane z kapitálových výnosov (KESt). KESt je špeciálna forma zrážkovej dane, ktorá sa priamo zráža z banky alebo platobného agenta a odvedie na daňový úrad.

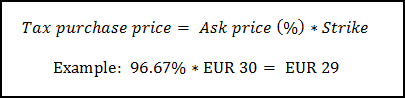

V prípade splatenia reverzne konvertibilného dlhopisu formou dodávky je dôležitá daňová nákupná cena dodaných akcií:

- Ak bol reverzne konvertibilný dlhopis zakúpený počas upisovacieho obdobia (= primárny trh), ako nákupná cena sa použije strike cena (uzatváracia cena akcie, ktorá sa má dodať k úvodnému dňu ocenenia). Tým pádom sú cenové výnosy z akcie až do úrovne strike ceny oslobodené od KESt.

- Ak sa nákup certifikátu uskutočnil na sekundárnom trhu, na výpočet daňovej nákupnej ceny akcie sa použije predajná cena v čase nákupu:

Precenenie akcie až do výšky vypočítanej ceny (súčin nákupnej ceny a strike ceny) je oslobodené od dane.

Iné typy certifikátov

Tento efekt sa dá vysvetliť takzvanou „závislosťou od vývoja“. Výkonnosť faktorového certifikátu je spojená s výkonnosťou podkladového aktíva, pričom denná výkonnosť certifikátu sa rovná percentuálnej zmene hodnoty podkladového aktíva vynásobenejpákovým faktorom stanoveným pri emisii (bez vplyvu úrokovej sadzby). Faktor pákového efektu zostáva konštantný počas celej doby splatnosti.

Závislosť od vývoja možno ilustrovať na nasledujúcom príklade s exemplárnym faktorovým certifikátom Long s faktorom 3 na ropu: Kvôli prehľadnosti predpokladajme, že podkladová ropa aj certifikát majú v prvý deň hodnotu 100 USD. Ak napríklad podkladové aktívum v jeden deň klesne o dve percentá (zo 100 USD na 98 USD) a potom sa v nasledujúci deň zotaví o ekvivalent 2 USD (čo sa rovná 2,04 %), cena ropy dosiahne pôvodnú úroveň 100 USD.

Faktorový certifikát však stráca peniaze: v prvý deň certifikát faktora 3 vynáša 6 % (bez menových vplyvov) zo 100 USD na 94 USD. Nasledujúci deň získava presne trikrát 2,04 % (= 6,12 %), a tak stúpa na 99,75 USD. Investor tak utrpí stratu približne 0,25 %, hoci cena podkladového aktíva/ ropy sa nezmenila.

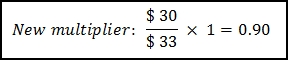

Upisovací pomer udáva, nakoľko jednotiek podkladového aktíva sa certifikát vzťahuje. Pomer 0,01 alebo 1:100 teda znamená, že na reprezentáciu jednej jednotky podkladového aktíva potrebujete 100 certifikátov.

Všetky investičné možnosti pre komoditu ropa (napr. certifikáty, fondy, ETC) sú vždy založené na cene ropy obchodovanej na futures trhu („futures kontrakt“). Dôvod je zrejmý: aby mohol emitent ponúkať produkty na ropu, musí byť schopný obchodovať s podkladovým aktívom ako so zabezpečovacou transakciou. Keďže však finančné inštitúcie nedisponujú vhodnou kapacitou na skladovanie ropy, produkty na fyzickú ropu nie je možné ponúkať. Riešením je obchádzka cez trh s futures, kde sa s ropou s rôznymi trvaniami dodania môže obchodovať ako s finančným nástrojom.

Naše „otvorené“ participačné certifikáty sú založené na podkladovom futures kontrakte s najkratším zostávajúcim trvaním. Pred vypršaním platnosti futures sa musia vždy preklopiť do ďalšieho termínu splatnosti, aby sa predišlo fyzickému dodaniu podkladového aktíva. To znamená, že sa nakúpi futures kontrakt, ktorému končí trvanie, a nasledujúci termín splatnosti. Aby sa zabránilo skokovému nárastu ceny certifikátu počas procesu preklopenia, upraví sa upisovací pomer. Ak je nasledujúci splatný futures kontrakt drahší ako ten, ktorému končí trvanie, dostanete z tohto kontraktu „menej“ - upisovací pomer sa zníži.

Príklad:

Predpokladajme, že pomer je v súčasnosti 1:1, t. j. certifikát zodpovedá presne jednej jednotke podkladového aktíva, pričom nasledujúci futures kontrakt stojí 33 USD a končiaci 30 USD:

V tomto príklade by sa preto upisovací pomer znížil z 1 na 0,90.

Investori sa podieľajú 1:1 na future s najkratšou zostávajúcou splatnosťou medzi jednotlivými výkyvmi. Ak sa future pohybuje medzi jednotlivými pólmi, cena certifikátu sa nezmení, pretože zmena bude neutralizovaná úpravou pomeru. V dôsledku procesu preklopenia teda investor nezískava výnos, ale zároveň nie je vystavený strate.

Máte ďalšie otázky týkajúce sa certifikátov?

Ďalšie otázky vám radi zodpovieme v našej sekcii Často kladené otázky a podrobne na ne odpovieme.

Svoju otázku pošlite na adresu

info(at)raiffeisencertificates.com

Váš tím Raiffeisen certifikáty